The word “tariff” used to feel like something reserved for economics textbooks and dry policy briefings. Not anymore. Since 2025, tariffs have moved into everyday conversations, boardroom emergencies, and front-page headlines – and in 2026, the ripple effects are still spreading. Some businesses are bleeding. Others are quietly placing bets on a very different future.

The story here is not simple, and honestly, that’s what makes it so fascinating. We’re watching an unprecedented reshaping of entire industries, some crumbling under the pressure, some being forced to adapt at breakneck speed. Let’s dive into what’s really happening – and which sectors you should be watching most closely right now.

The Scale of What We’re Dealing With

Let’s be real about the size of this thing first. President Trump’s historically unprecedented tariff increases raised U.S. trade protectionism to the highest level in at least 80 years. That’s not a small shift in policy – that’s a structural earthquake for global commerce. The shockwaves are still moving through supply chains, pricing models, and employment numbers in ways that are only now becoming fully visible.

The Trump tariffs are the largest U.S. tax increase as a percent of GDP since 1993 and amount to an average tax increase per U.S. household of roughly $1,500 in 2026. Think about that for a moment. This isn’t abstract economic policy. It’s money coming directly out of the pockets of ordinary consumers, which will inevitably squeeze demand across a wide range of goods and services.

Oxford Economics downgraded its global industrial growth forecast from around two and a half percent to under two percent in both 2025 and 2026, with the largest forecast downgrades in the U.S., where manufacturing activity is expected to contract by roughly one percent in 2026. That kind of coordinated global slowdown is the kind of backdrop against which entire industries can buckle if they’re already financially stretched.

Industry at Risk No. 1 – The Automotive Sector Under Siege

If you want to understand just how badly tariffs can gut an industry, look no further than auto manufacturing. Tariff costs for automakers have reached at least $35.4 billion since 2025, when President Trump implemented new tariffs on imports of vehicles, parts, steel, and aluminum. That figure alone should stop you in your tracks. Thirty-five billion dollars. Gone. And it keeps climbing.

An April estimate from Michigan’s Center for Automotive Research suggested that Trump’s Section 232 tariffs would combine to cost manufacturers, distributors and customers about $108 billion across the U.S. auto industry, with $42 billion falling on the Detroit Three automakers – nearly triple their combined 2024 profits. Triple. That’s not a headwind. That’s a wall.

The automotive industry is highly globalized, with nearly half of the vehicles sold in the U.S. manufactured outside of the country, and the most challenging aspect of this tariff cycle has been the constant, on-again-off-again nature of the policies. That unpredictability is its own form of damage, making it nearly impossible for auto executives to plan investments, set prices, or manage their supply chains with any confidence. Vehicle prices inched to record highs in 2025, and while industry experts worry automakers will eventually cave to cost pressures, one auto consultant’s outlook for 2026 projects only 15.6 million vehicle sales, down from 16.2 million the year before.

The Auto Parts Chain – A Crisis Within the Crisis

In 2024, the U.S. imported $217 billion worth of cars from countries like Mexico, Canada, Japan, South Korea, and Europe, including $49.7 billion from Mexico and $28.3 billion from Canada alone. These aren’t minor supply lines – these are the arteries of a deeply integrated continental manufacturing ecosystem. When you tariff them, you don’t just make cars more expensive. You destabilize hundreds of smaller component suppliers who have almost no margin to absorb extra costs.

Even vehicles assembled in the U.S. are feeling the squeeze, with tariffs on steel, aluminum, copper, parts, and battery materials driving up costs for automakers and auto dealers. So the “just build it here” argument, which sounds logical in a White House briefing, doesn’t hold up when the inputs themselves are all subject to heavy duties. There’s no domestic island in this supply chain.

Volvo Cars announced plans to cut 3,000 jobs globally as part of a nearly $1.9 billion cost-cutting initiative, reflecting increasing challenges in the global market, including tariff pressures, and prompting the company to withdraw its financial guidance for 2025 and 2026. Volkswagen raised starting prices on most of its 2026 models by as much as six and a half percent. I think we’re only seeing the beginning of how this supply chain crisis cascades into showrooms and into workers’ paychecks.

Industry at Risk No. 2 – Pharmaceuticals on the Brink

Here’s the thing about the pharmaceutical industry: it didn’t start this year in tariff trouble. Most drugs and drug ingredients were initially exempted. While pharmaceuticals and certain APIs were initially exempted from the reciprocal and base import tariffs in early April 2025, Commerce Secretary Howard Lutnick indicated that industry-specific tariffs potentially exceeding 25 percent are on the horizon, and the administration’s Section 232 investigation could introduce even broader restrictions based on national security justifications. The exemption window is closing – fast.

The United States imported $225 billion of pharmaceutical products and ingredients in 2024, and if the Trump administration takes action to impose tariffs on pharmaceuticals in 2026, higher tariff costs could range from $19.7 billion to $23 billion. That is a colossal cost increase hitting an industry where prices are already politically explosive. Passing those costs onto patients? Good luck.

Even before full tariff implementation, companies anticipated disruption: there was already a 70 percent increase in medicine imports and a staggering nearly 500 percent increase in basic pharmaceutical product imports as firms rushed to front-load inventory. That kind of panic stockpiling signals deep anxiety. Tariffs can create supply chain disruptions, increase costs, limit patient access to essential medications, and negatively impact research and innovation. When we’re talking about patient access to medicine, this stops being just an economic argument and becomes something far more serious.

The Pharma Supply Chain’s Hidden Vulnerability

Given that roughly three-quarters of U.S. medical devices are manufactured abroad – primarily in China, Mexico, and Canada – further tariffs risk increasing costs and causing shortages of critical equipment. It’s hard to overstate how fragile this is. The assumption for decades has been that global pharma supply chains are so sophisticated and diversified that no single policy shock could break them. That assumption is now being seriously tested.

The Trump administration has signaled that tariffs on pharmaceuticals could potentially rise toward 200 percent by mid- to late-2026. Two hundred percent. Even the mention of that number sends a shiver through the entire global pharma ecosystem. Reality shows that switching pharmaceutical production back to the U.S. requires long timelines of five to ten years or more and high investments, due to the specialized and regulated nature of pharmaceutical manufacturing.

PwC’s tariff industry analysis finds that total tariff measures could increase from just $0.5 billion a year to nearly $63 billion a year for the Pharmaceutical, Life Science, and Medical Device industry under the proposed frameworks. That’s not a bump in the road. That’s the road disappearing. Risks of cost increases, supply shortages, and innovation slowdowns may well outweigh the short- and medium-term gains in domestic production.

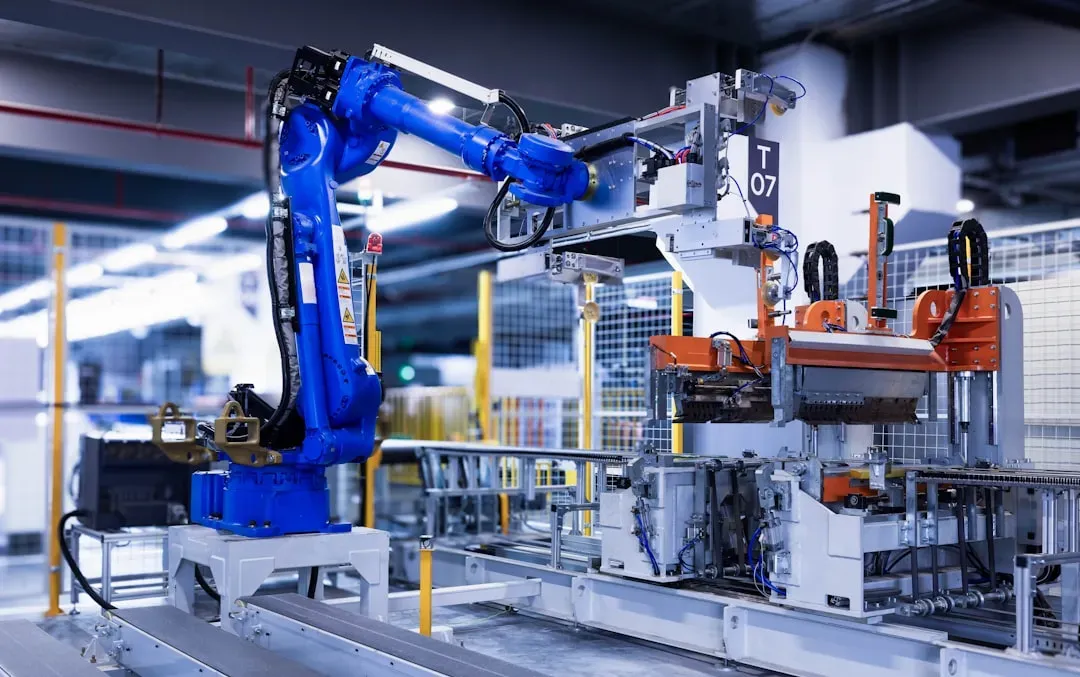

The 1 Industry That Could Actually Surge – Domestic Manufacturing and Automation

Alright. Not everything in this story is grim. Here’s where it gets genuinely interesting. While import-dependent sectors are reeling, domestic manufacturers, particularly those tied to automation and reindustrialization, are staring at an opportunity that hasn’t existed in decades. In 2026, the tariffs are propelling a structural reset in U.S. manufacturing that’s been overdue for decades, and the tariff environment of 2025 has led to what analysts describe as the clearest runway for U.S. reindustrialization in decades.

There is already a giant surge in engineering demand, which is the earliest indicator of expansion – because engineering precedes construction, automation installations, and equipment purchases, and when engineering pipelines fill up, it means companies are preparing to build. This is what economists call a leading indicator. It’s the kind of signal that, if you blink, you miss. Companies are quietly betting that domestic production capacity will be worth more in a tariff-heavy world than it ever was before.

Long-run output in the manufacturing sector is projected to expand by about three percent, with non-advanced durable manufacturing seeing the largest gains. And interestingly, manufacturing subsectors tied to primary metal production were among the few to actually add jobs in 2025, even as the broader sector contracted. It’s a classic case of creative destruction – painful at the macro level, but creating very real winners at the sub-sector level.

Automation, Reindustrialization, and Who Wins in a Tariff World

As production returns to the U.S., companies understand they cannot recreate the old factory model – the U.S. doesn’t have the labor base to double manufacturing headcount. The implication is clear: the next wave of American manufacturing will be driven by robots, automation systems, and AI-powered logistics – not the nostalgia of 1970s assembly lines. The companies positioned to supply and build that automated infrastructure stand to gain enormously.

In response to the vulnerabilities exposed by the trade war, the U.S. government accelerated efforts to reshore defense manufacturing, using the Defense Production Act to incentivize domestic production of semiconductors, rare earth processing, and advanced composites. Defense-adjacent manufacturers are seeing investment flows that were virtually non-existent five years ago. The defense industry now leans toward diversified sourcing, modular platform design, and regional manufacturing nodes, with the reshoring momentum continuing, aided by automation and AI-enabled supply chain optimization.

It’s hard to say for sure how quickly this reindustrialization plays out – building new factories takes years, skilled labor is still scarce, and tariff policy remains volatile. But companies should expect continued movement in tariffs, growing export control restrictions, and trade enforcement investigations with long-term implications for supply chains, investment strategy, compliance planning, and commercial contracting. The businesses that build for that reality now, rather than hoping for a return to the pre-2025 trade environment, will be the ones writing the success stories of the next decade.

Conclusion: A Crossroads Nobody Planned For

We are living through a genuinely historic restructuring of global trade. Tariffs are being deployed as a tool for both economic leverage and national security objectives, affecting a wide range of goods and industries. The auto industry is absorbing tens of billions in extra costs while trying to pass as little as possible to consumers who are already stretched thin. Pharmaceuticals are staring down the barrel of a tariff regime that could hit nearly $63 billion and disrupt drug supply chains built over generations.

Meanwhile, domestic manufacturers and automation companies are quietly entering what could be their most significant growth cycle in modern history. Whether tariffs will succeed in increasing manufacturing jobs and wages, or reshoring strategic industries, remains an open question – it may simply be too soon to know. The answers will become clearer as 2026 unfolds, but the sides are already being chosen.

The irony of this entire tariff era might be this: the policies designed to protect American workers are simultaneously threatening some of the industries those workers depend on, while accidentally creating a powerful tailwind for a new generation of highly automated domestic production. The question isn’t just which industries survive. It’s which ones you’re in – and what you’re going to do about it now. What would you have guessed was coming?