There’s a quiet tension running through many middle-class households right now. Incomes look decent on paper, jobs are held, bills get paid more or less on time. Yet a growing body of research suggests that a stable paycheck does not automatically translate to financial security. A “middle class” income no longer guarantees financial security, threatening both the nation’s economy and its social fabric, according to a 2024 report from the Financial Health Network.

What often drives this vulnerability isn’t bad luck alone. It’s a set of everyday habits that feel perfectly normal, even prudent, but gradually erode the financial foundation beneath a family’s feet. Middle-class families face unique financial challenges in today’s economy. While they earn decent incomes, they often struggle to build lasting wealth due to subtle but destructive money habits. These seemingly minor financial decisions compound over time, creating barriers to economic security and limiting opportunities for wealth accumulation. Here are fifteen of the most common ones worth examining closely.

1. Spending First and Saving Whatever Is Left

The middle class tends to spend first and save whatever remains. Since expenses expand to fill available income, nothing remains. Without automatic investing, wealth building never begins. This pattern might not feel dangerous in the short term, but over a decade it represents a serious drag on long-term financial health.

Only about half of middle-class households are putting money into a savings account at all. The fix is straightforward in concept but difficult in practice: treat savings like a fixed bill rather than an afterthought. Automating contributions to retirement accounts or an emergency fund before discretionary spending begins is one of the most reliable ways to break the cycle.

2. Carrying High-Interest Credit Card Debt

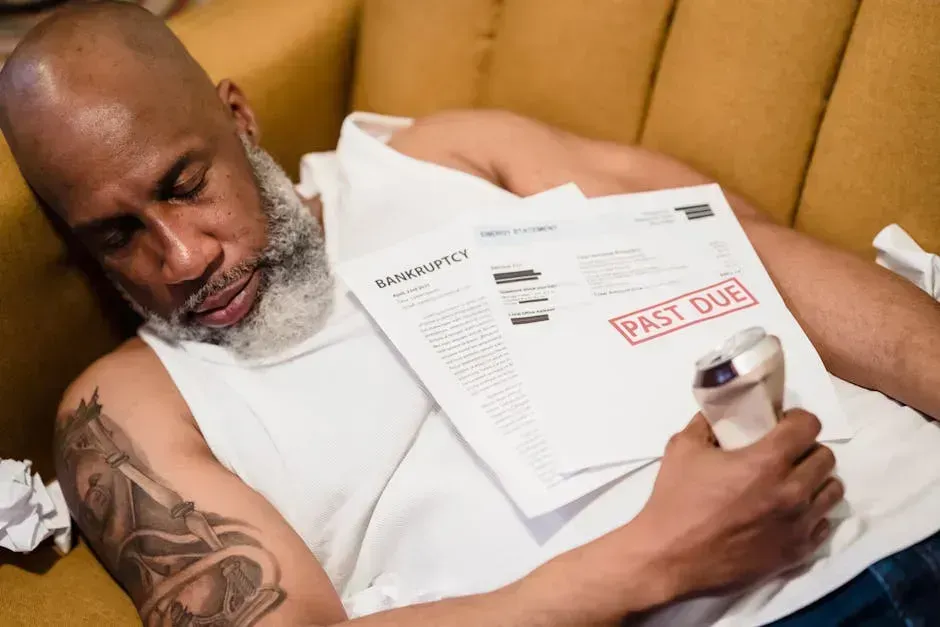

Credit card debt represents one of the most wealth-destroying habits for middle-class families. With interest rates typically ranging from 18% to 29%, carrying balances means paying hundreds or thousands of dollars annually in interest charges. The minimum payment structure designed by credit card companies keeps borrowers trapped in debt for years or even decades.

Total US credit card balances hit a record $1.28 trillion at the end of 2025, per the NY Fed. Split across balance-carrying households, that’s roughly $10,000 per household. At 20-plus percent APRs, that’s over $2,000 a year just in interest. That figure represents money that could otherwise be building an emergency fund, contributing to retirement, or simply reducing financial stress.

3. Living Without an Emergency Fund

Living without an emergency fund leaves middle-class families vulnerable to financial catastrophe. When unexpected expenses arise, families without savings must rely on credit cards, high-interest loans, or borrowing from retirement accounts. This creates a dangerous cycle where financial setbacks become increasingly difficult to recover from.

Almost four in ten middle-class households are not confident that they could pay an unexpected expense of $5,000 and bounce back financially. A lack of emergency savings is a sign of short-term thinking. According to a study by the Consumer Financial Protection Bureau, nearly four in ten households could only cover expenses for a month or less in case of an income interruption. A car repair or a medical copay becomes a genuine crisis rather than a manageable inconvenience.

4. Lifestyle Inflation After a Pay Raise

A significant barrier for the middle class in growing wealth is not paying attention to lifestyle inflation, also known as lifestyle creep. This is when, as individuals earn more, they increase their spending proportionally, or even excessively, which can stymie their ability to save and invest in a more suitable fashion.

Lifestyle inflation occurs when people spend more as their income increases. This phenomenon has plagued millions of middle-class families during the post-pandemic era. While average wages rose significantly between January 2020 and January 2024, the personal savings rate fell from 7.2% to 4% during the same time. This pattern means that even though you are making more, you are not actually saving any more than before. It is a treadmill that keeps you running in place, no matter how much progress you make in your career.

5. Neglecting Retirement Contributions

Failing to prioritize retirement savings represents a critical mistake that becomes increasingly expensive with time. Many middle-class workers delay retirement contributions, believing they can make up for lost time later in their careers. The compounding math on those delayed years is punishing in ways most people underestimate.

Full-time workers cut their retirement contribution rate in 2025 to 8.9%, from 9.2% a year earlier, while one in four workers reduced their annual savings in their 401(k) or other types of employer-sponsored accounts. Almost half of middle-class households report they are not confident they will be able to build sufficient retirement savings. Missing even a few years of compounding growth early in a career can mean a significantly smaller nest egg at retirement.

6. Subscription Creep Going Unnoticed

According to Consumer Affairs, subscription creep got expensive as 2025 dragged on. Many households paid 15% to 30% more per month for the subscriptions that they held. Consumers continued to pay companies for unwanted monthly or annual memberships even when prices increased, often on short notice or without much disclosure.

Food delivery services, streaming subscriptions, housekeeping, meal kits, premium apps, car washes, lawn care – convenience purchases add up quickly. These services aren’t necessarily wrong, but middle-class earners rarely track their cumulative cost. Spending $400 to $600 monthly on convenience means $4,800 to $7,200 annually, which doesn’t contribute to building wealth. That’s a meaningful sum quietly departing the household every single year.

7. Buying Brand-New Vehicles

Purchasing a new vehicle represents one of the most significant financial mistakes made by middle-class Americans. After driving off the dealership lot, a brand-new car loses approximately 9% of its value within the first minute. New vehicles depreciate quickly, losing 20% of their value in the first year. This rapid depreciation continues relentlessly, with the average new car losing about 15% of its value yearly until it hits the five-year mark.

Transportation costs represent a significant portion of middle-class budgets, and poor car-buying decisions can devastate financial progress. Many families purchase vehicles based on monthly payment affordability rather than total cost or their actual transportation needs. Extended loan terms make expensive cars appear affordable while maximizing the total interest paid. A vehicle that’s two to three years old is often a smarter choice. The original owner has already absorbed the steepest depreciation hit, while you get a nearly new car at a fraction of the price. The savings difference, often $10,000 or more, could be invested instead.

8. Oversizing the Home

Housing represents the most significant expense for most middle-class households, and the trend toward increasingly larger homes has become a financial anchor for many families. The American tendency to constantly upgrade to bigger homes as income increases creates a dangerous cycle that undermines long-term financial security.

The financial impact of upsizing is substantial. A family moving from a $300,000 home to a $500,000 property might face an additional $1,000 in monthly expenses between increased mortgage payments, property taxes, insurance, utilities, and maintenance. That’s $12,000 annually – money that could instead fund retirement accounts, college savings, or other investments. Middle-class households already spend an average of $55,900 per year, with housing alone consuming roughly a third of that budget.

9. Ignoring a Written Budget

If you don’t know where your money goes, you can’t control where it goes. Most middle-class earners have only a vague sense of their spending. They know major bills, but can’t account for thousands in discretionary expenses. Without tracking, money leaks everywhere. Restaurant meals, online shopping, subscription renewals, impulse purchases, and forgotten services all drain accounts invisibly.

Living without a budget means you don’t have a roadmap for where your money will go. It isn’t about restriction for its own sake. A realistic budget simply reveals where trade-offs are being made unconsciously, which gives families the option to make those choices deliberately rather than by default. The information alone often changes behavior.

10. Being Underinsured

Many households remain underinsured, with survey data noting that those with children under 18 are no more likely than other middle-class households to say they maintain life insurance coverage, at roughly one in three. Health insurance gaps can lead to medical bankruptcies that wipe out years of financial progress. Life insurance protects dependents from financial hardship if the primary income earner dies. Property insurance protects against losses from natural disasters or accidents. Proper insurance has minimal coverage costs compared to the potential financial devastation caused by being underinsured when disaster strikes.

Roughly four in ten middle-class households are not confident they will be financially protected in the event of a major medical expense, the need for long-term care, or the unexpected death of an income-earner. Insurance feels like a monthly cost until the moment it becomes the only thing standing between a family and financial ruin. Treating it as optional is a gamble with exceptionally poor odds.

11. Skipping an Estate Plan

With the federal estate tax exemption set at $13.99 million per individual in 2025, many families assume estate planning is only relevant to the ultra-wealthy. This common misconception can lead to serious gaps in protection, costly legal delays, and missed opportunities for control and care. A will, a basic trust, or even a simple beneficiary update can protect a family’s assets in ways that income alone cannot.

One of the most common estate planning errors is neglecting to update documents as life circumstances change. Major life events such as marriage, divorce, the birth of children, or the death of a loved one should prompt an immediate review of your estate plan. Without these steps, assets may not reach the intended people, and the family left behind can spend months or years in costly legal proceedings that deplete the very estate they were meant to inherit.

12. Tapping Retirement Accounts for Short-Term Needs

Research from Vanguard found that a record share of Americans tapped their retirement savings accounts to cover emergency expenses. In 2025, 6% of people enrolled in 401(k) plans managed by Vanguard made so-called hardship withdrawals from their accounts, up from 5% in 2024. These withdrawals typically trigger taxes and early withdrawal penalties, which can reduce the amount received by more than a third.

Beyond the immediate tax hit, the long-term damage is worse. Money pulled from a retirement account at age 40 is not just the dollar amount withdrawn. It’s every dollar that money would have compounded into over the following two to three decades. Failing to grasp compound returns means underestimating how small investments grow over decades. That gap can be enormous by the time retirement arrives.

13. Focusing on Monthly Payments Instead of Total Cost

The monthly payment mindset obscures the actual cost of purchases and encourages overspending. It also chains your future income to past decisions. When half your monthly income goes to service payments for cars, furniture, and electronics, you’ve eliminated your financial flexibility. You can’t invest, can’t save, and can’t handle emergencies without adding more debt. The monthly payment mentality guarantees staying broke because it prioritizes short-term affordability over long-term wealth.

This thinking shows up most clearly in car buying and consumer finance offers, but it also applies to home upgrades, furniture, and appliances purchased through zero-interest promotional plans. It is easy to say yes to a “zero percent interest” offer on a new sofa or a high-tech gadget for your home. The danger is that these payments stack on top of each other until very little of a paycheck remains unspoken for.

14. Neglecting Financial Literacy

Many middle-class earners don’t understand how tax brackets work, what investment returns mean, or how employer retirement matches function. This ignorance costs thousands annually. Missing a 401(k) match means rejecting free money. Not understanding how contributions reduce taxable income means paying more to the IRS.

These aren’t complex topics, but the middle class tends to avoid learning them. That avoidance is expensive. The difference between optimized and ignored retirement planning can easily exceed $500,000 over the course of a career. A few hours spent understanding employer benefits, tax-advantaged accounts, and basic investing principles consistently pays better returns than almost any single financial product available.

15. Financially Supporting Adult Children at the Expense of Retirement

One frequent mistake that middle-class families make is taking care of their grown children’s bills, such as rent or healthcare, when nearing retirement. To avoid falling into this parental money pit, teaching kids financial independence is essential. If you stop funding their lifestyle, you can start funding a more comfortable retirement plan.

Silent spending habits like subscription overload, helping adult kids, lifestyle creep and ignoring fees can hurt retirement savings and financial future. There is real emotional difficulty in setting these boundaries, particularly when adult children are genuinely struggling. Still, parents who consistently redirect their own retirement savings toward grown children’s living costs may find themselves financially dependent in their own old age, which creates a heavier burden on the next generation rather than resolving one. Many middle-class households are walking a financial tightrope where one unexpected event, like a job loss or major expense, could throw their stability into question. They often lack the financial cushion available to higher-income families, yet their income and asset levels place them outside the reach of government safety net programs designed for lower-income households. This gap can create a deep sense of financial vulnerability. Recognizing which habits contribute to that gap is the first step toward closing it.